Introduction

In October 2021, the Petroleum Products (Taxes and Levies) (Amendment) Bill 2021 (hereinafter ‘the Bill’) was tabled in the National Assembly by the Departmental Committee on Finance and National Planning. The Bill, if enacted, would introduce various changes to the petroleum pricing framework in Kenya.

The Bill was introduced amid concerns regarding the drastic increment in prices of petroleum and petroleum products in the last year, which reached an unprecedented high in September 2021. Against this backdrop, Parliament, through the Committee on Finance and National Planning, received petitions from consumers and other stakeholders affected by the drastic increment in the prices of petroleum products. The Committee thereafter prepared and tabled the draft bill proposing legislative amendments in line with the recommendations made by the petitioners. The Bill is now available for comments after having been approved for publication by the Speaker of the National Assembly.

Petroleum is indeed the fuel that runs the economy. It plays a critical role in industrial production, transportation, generation of electricity amongst other uses. As such, a rise in the cost of petroleum products will have a ripple effect on these sectors which, on the whole, raises the cost of doing business and the cost of living, hence the general concern.

In this alert, we delve into the proposed legislative amendments. We begin with an overview of the pricing model in Kenya and conclude with a brief analysis of the proposed amendments.

1. An overview of petroleum pricing in Kenya

Petroleum pricing in Kenya is currently regulated by the Energy (Petroleum Pricing) Regulations 2010 (hereinafter ‘the Regulations’). The Regulations prescribe a formula that is used by the Energy and Petroleum Regulatory Authority (‘EPRA’) to determine the maximum wholesale price and retail pump price of super petrol, diesel, and kerosene. The prices come into effect on the 15th day of every calendar month and remain in force until the 14th day of the following calendar month.

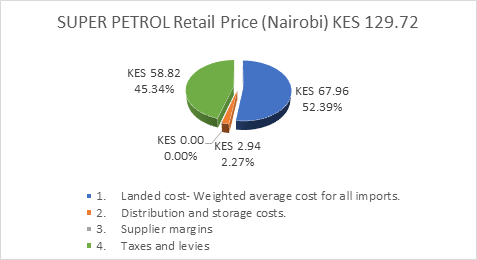

The following items constitute the basic cost components of the maximum retail price:

(a) The Landed costs

The landed cost is the weighted average cost (per product) of super petrol, diesel, and kerosene. Kenya sources the larger percentage of its crude oil from the Murban Crude Oil marketed by the Abu Dhabi National Oil Company (ADNOC). When ADNOC sets the monthly price of crude oil for a specific month, this becomes the basis of the free on board (FOB) loading port price for the market supply tenders issued in Kenya under the Open Tender System (OTS). The OTS is a system where licensed Oil Marketing Companies bid to import petroleum products into Kenya for the whole market at the lowest price. The winning company then on-sells the imported product to other Oil Marketing Companies at the winning bid price plus industry agreed cost build-up parameters to land the product into Kenya. (ref https://www.pwc.com/ke/en/assets/pdf/petroleum-sector-master-plan-for-kenya.pdf). In terms of Regulation 7 of the Energy (Petroleum Pricing) Regulations 2010 the unit cost of the product is the landed cost, plus refinery fees for the month’s crude imports at the Kenya Petroleum Refineries Limited.

(b) Taxes and levies

The following taxes and levies are imposed on petroleum products in Kenya:

| Tax and/or Levy | Super Petrol | Diesel | Kerosene |

| a) Excise Duty | 21.95 | 11.37 | 11.37 |

| b) Road Maintenance Levy (Road Maintenance Levy Fund Act, No. 9 of 1993) | 18.00 | 18.00 | – |

| c) Petroleum Development Levy (Petroleum Development Levy Fund Act, No. 4 of 1991)* | 5.40 | 5.40 | 0.40 |

| d) Petroleum Regulation Levy | |||

| e) Anti-adulteration Levy (Section 8A of the Miscellaneous Fees and Levies Act, No. 29 of 2016) | – | – | 18.00 (on customs value) |

| f) Merchant Shipping Levy | |||

| g) Import Declaration Fee | |||

| h) Value Added Tax † | 9.61 | 8.19 | 7.67 |

Note:

*The Act establishes a Petroleum Development Fund. The apparent policy intention for the imposition of the levy was to use the funds collected for price stabilization in the event of price hikes in international crude oil. However, the Act only provides, in Section 4 (4) that funds collected from the levy will be used as necessary for the development of common facilities for the distribution or testing of oil products and for matters relating to the development of oil industry as the Cabinet Secretary may direct.

†Value Added Tax (‘VAT’) which is presently imposed at Kshs. 9.61 per litre on super petrol, Kshs. 8.19 per litre on diesel and Kshs. 7.67 per litre on kerosene. Under the Value Added Tax Act 2013 (‘VAT Act 2013’), VAT on a specific list of petroleum products was originally exempt. This was to be the case for a period of 3 years from the time the VAT Act 2013 became law, which was 2nd September 2013. A further two years extension was granted under the Finance Act 2016, and effective 1st September 2018 a 16% rate VAT was reintroduced on the petroleum products. The Finance Act 2018 reduced this percentage to 8% which was a welcome move. However, the Tax Laws (Amendment) Act 2020 then increased the vatable base of petroleum products to include excise duty, fees and other charges which were previously excluded from the VAT value.

(c) Oil marketing companies’ margins

Oil marketing companies’ margins refer to the wholesale and retail margins allowed to Oil Marketing Companies and retail dealers. Wholesale margins allow oil marketing companies to recover the operating costs and remit investments in wholesale activities relating to the marketing of petroleum products.

Retail margins allow for recovery of the operating costs and remit investments in a retail service station. The Regulations allow a maximum wholesale margin of Kshs. 6.00 per litre and a maximum retail margin of Kshs. 3.00 per litre.

(d) Storage and distribution costs

Storage costs largely include the cost of utilizing the Kipevu Oil Storage facility which is the government-owned tank farm for imported refined oil products. The costs are provided in the First Schedule to the Regulations. Transportation and distribution costs include costs of transporting petroleum products from Mombasa to the nearest wholesale depot, and from the nearest wholesale depot to a retail dispensing site.

In this connection, the Regulations allow for the recovery of maximum operational losses at the pipeline at 0.25% for all petroleum products, and for the recovery of maximum operations losses at the depot at 0.5% for super petrol and diesel, and 0.3% for kerosene.

Breakdown of retail price by cost components as at 14th December 2021

2. Proposed amendments under the Petroleum Products’ (Taxes and Levies) (Amendment) Bill 2021

The Bill proposes to revoke the Energy (Petroleum Pricing) Regulations 2010. As such, the Bill introduces a Sixth Schedule to the Energy Act 2019 which prescribes the pricing formula for petroleum products. The Bill allows the Cabinet Secretary to review the formula prescribed in this schedule by notice in the Kenya Gazette, on condition that this notice is laid before the National Assembly within seven days of publication for approval. The National Assembly will then approve or reject the proposal within twenty-eight (28) sitting days from the date of receipt of the notice.

This was previously a prerogative entrusted solely to the Energy Regulatory Commission (now EPRA). This change would ensure more accountability in the review of the formulae for petroleum pricing.

The Bill also proposes to introduce the following notable changes:

(a) The Bill proposes to lower the maximum allowed operational losses at the pipeline and depot to 0.01%, currently 0.25% at pipeline and 0.50% at depot. These losses have to be recovered in the retail petroleum price charged to consumers. This would effectively lower the amount that consumers must pay for losses incurred, especially if losses are occasioned by system inefficiencies that have little connection with the actual cost of petroleum products.

(b) The Bill provides for maximum allowed margins at Kshs. 9.00 per litre for super petrol, regular petrol, kerosene, and automotive diesel. The Bill would effectively retain the maximum allowed margins as they stand in the Regulations, considering the maximum allowed margins for wholesale activities (at Kshs. 6.00 per litre) and retail activities (at Kshs. 3.00 per litre) give a maximum total of Kshs. 9.00 per litre.

It bears noting that there is no clarity in the current legal or policy regime on how the maximum allowed margins are arrived at. They therefore place a cap on the amount that Oil Marketing Companies can recover in operating costs that may not reflect the actual costs incurred by the companies. Therefore, in the interests of transparency and accountability, it will be important that Parliament provide clarity on the basis for the maximum allowed margins provided for in the draft Bill.

(c) The Bill proposes to amend Section 10 of the Excise Duty Act, No 23 of 2015. This section allowed the Commissioner-General of the Kenya Revenue Authority to adjust the specific rate of excise duty for goods and services once every year to factor for inflation. The rate of excise duty is now to be adjusted every two years taking into account the rate of inflation. However, this will not apply to the following petroleum products:

1. Motor spirit (gasoline) premium;

2. Illuminating kerosene;

3. Gas oil (automotive, light, amber for light speed engines); and

4. Diesel oil (industrial heavy, black, for law speed marine and stationery engines).

This suggests that the excise duty rates for the above products will remain fixed, although it is unclear if this interpretation is accurate. It will be important for the regulator and tax authorities to clarify what effect this provision will have on the rate of excise duty for the above products.

(d) The Bill further proposes to introduce the following amendments to the Petroleum Development Levy Fund Act, No. 4 of 1991:

1. The Bill proposes to introduce a new ‘Section 3’ to the Act with, inter alia, the following provisions:

(a) The Bill introduces a new schedule to the Act. The schedule provides a rate at which the Petroleum Development Levy will be imposed for the list of petroleum products provided in the First Schedule.

(b) The levy will be paid into the Petroleum Development Fund.

(c) Oil marketing companies will be required to be registered as remitters of the fund with the collector and pay the levy immediately upon importation of petroleum fuel or at the time of its delivery from the refinery.

2. Notably, the Bill now expressly provides for the purpose of levy, which shall be used for:

(a) Matters relating to the development of the oil industry;

(b) Development of common petroleum facilities for distribution or testing of oil products;

(c) Stabilization of local pump prices in instances of spikes occasioned by high landed costs above a threshold determined by EPRA.

While this provides more clarity relative to the current regime, it may be advisable to separate the role of ‘development’ from ‘price stabilization’. This will ensure more accountability in the use of funds.

3. The Bill proposes to establish a Petroleum Development Fund Advisory Board comprising a Cabinet Secretary responsible for Finance, a Cabinet Secretary responsible for Energy, a Cabinet Secretary responsible for Petroleum and a representative of EPRA. While the Cabinet Secretary in charge of petroleum will be permitted to draw down funds from the Petroleum Development Levy Fund for purposes of petroleum price stabilization, they will be required to seek the consent of the Advisory Board. The Advisory Board may further impose conditions on the use of any expenditure drawn down.

4. The Bill proposes to revoke the Petroleum Development Levy Order, 2020 (Legal Notice No. 124 dated 10th July 2020). It had increased the Petroleum Development Levy for both Super Petrol and Diesel by Kshs. 5.00 which made a significant contribution to the increase in the overall price of petroleum products.

This change will be a welcome move as it would significantly lower the overall cost of super petrol and diesel.

(e) The Bill proposes to introduce a provision in the Statutory Instruments Act 2013 requiring that any statutory instruments containing provisions dealing taxes, levies, and fees or which have the effect of imposing a charge on a public fund to be notified to the National Assembly. This will be within seven (7) days of being published in the Kenya Gazette. Within twenty-eight (28) sitting days of receiving the notice, the National Assembly will determine whether or not to approve the change.

This amendment is a welcome provision as it would prevent situations where a Cabinet Secretary unilaterally imposes taxes and levies without any form of accountability.

(f) Lastly, the Bill proposes to introduce an amendment to Section 5 (2) the VAT Act by reducing the VAT chargeable on the supply of petroleum products listed in Section B of Part 1 of the First Schedule from 8% to 4%. The Bill also proposes to charge VAT of 8% on the supply of liquefied petroleum gas including propane. This was formerly charged at 16% VAT.

This provision would be a welcome move as it reduces the cost of liquefied petroleum gas.

5. Conclusion

In many ways, the Bill introduces favourable amendments to the petroleum pricing framework in Kenya. Perhaps, more importantly, is the reduction of cumulative taxes and charges imposed on petroleum products. This was a prominent concern for consumers. Furthermore, the Bill promises more accountability in the imposition of taxes and levies and in the use of funds.

For more information and help in developing an Environmental, Social and Governance Framework and Implementation Strategy, please reach out to our Sustainability & Climate Change practice team or the Regulatory Compliance and Corporate Advisory practice team, through Partners Jinaro Kibet, Stephen Mallowah, or Head of Department, Bryan Muindi